Flying blind: European aviation hits new emissions high

The case for extending European carbon pricing to all departing flights

Downloads

Lead author

Executive summary

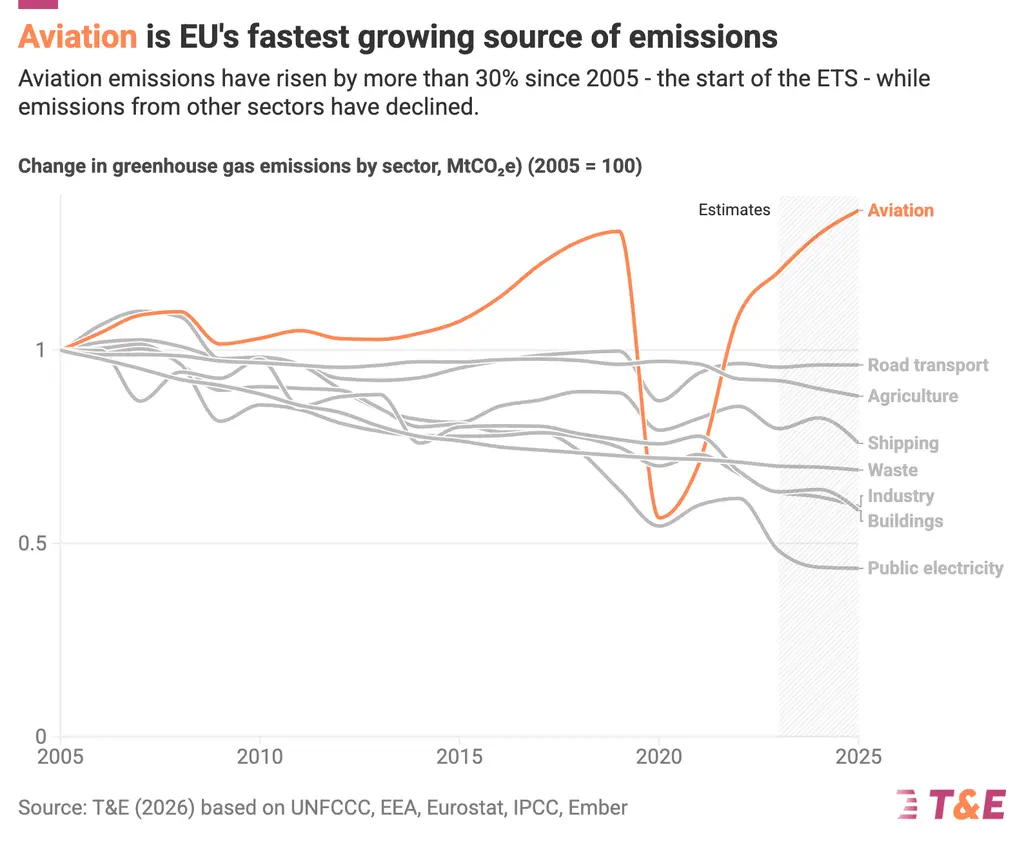

European aviation emissions surpassed pre-pandemic levels in 2025

In 2025, flights departing from European airports generated 195 Mt of CO₂, surpassing their 2019 level for the first time since the pandemic. Emissions rose 4% compared to 2024. This milestone is not cause for celebration. It confirms that the sector has rebuilt without cleaning up. Aviation remains the EU's fastest-growing source of emissions, having risen by more than 30% since 2005 while other sectors have cut theirs.

Europe is recovering faster than any other major market. Growth is concentrated among low-cost carriers: Ryanair's global emissions are now 50% above their 2019 level, the largest increase of any airline worldwide. Legacy carriers such as Lufthansa and Air France remain below pre-pandemic levels. Low-cost expansion, not legacy recovery, is driving European emissions back beyond their pre-pandemic peak.

Two-thirds of emissions escape carbon pricing

The carbon market remains structurally flawed. In 2025, 68% of emissions from European departing flights went unpriced, a consequence of the carbon market’s scope limitation to intra-European routes, leaving the most polluting long-haul routes entirely exempt. The effective price airlines paid per tonne of CO₂ resulted in a total of €23, far below the average EU ETS price of €73, paid for by other sectors.

None of the ten most polluting routes departing from Europe fall within the carbon market's scope. London-New York alone generated 1.4 Mt of CO₂, roughly equivalent to the annual tailpipe emissions of all cars in a city the size of Munich, yet it escaped any carbon pricing. The first route covered by the ETS appears only at 131st place in the global ranking: London-Milan, with 0.16 Mt of CO₂.

International offsetting through CORSIA is not a substitute for the carbon market

CORSIA, ICAO's global offsetting scheme for international aviation, is not a credible alternative to the EU’s carbon market. The scheme’s coverage is structurally limited and covers only a fraction of the EU aviation's CO₂ emissions. Many major aviation markets, including China and the United States, have not implemented it into national law. Its offsetting credits have serious environmental integrity concerns: the overwhelming majority of currently available credits derive from artificial adjustments that the UN review team found do not represent genuine emissions reductions. Unlike a cap-and-trade system, CORSIA sets no hard limit on emissions and provides no meaningful price signal for decarbonisation. The EU's assessment of CORSIA by 1 July 2026 should reflect this reality.

Extending carbon pricing can unlock billions for the green transition

Airlines avoided an estimated €8.5 billion in emissions costs in 2025 through scope exemptions and free allowances. Had the ETS applied to all departing flights, total revenues could have reached €12.7 billion, a threefold increase on what was actually collected in 2025. Extending the ETS to all departing flights would align the sector with the polluter pays principle and unlock significant revenue for public budgets. Total revenues could exceed €17 billion annually by 2030. Member States would be the primary beneficiaries, with some, including Poland, Czechia and Romania, gaining disproportionately due to the way general allowances are allocated.

We recommend that approximately 25% of these revenues be repurposed to accelerate the greening of the sector through three key measures:

-

Transform the Hydrogen Bank into a market intermediary to de-risk the transition to e-fuels via long-term purchase contracts.

-

Redesign SAF allowances to prioritise scalable e-SAF options and provide long-term revenue certainty for producers.

-

Establish a contrail allowance scheme using a small share of free ETS allowances to fund the operational costs of contrail avoidance, which could deliver massive climate benefits at a minimal cost to the industry.

The European Commission's 2026 revision of the carbon market is the moment to act. By closing the current pricing loopholes, Europe can ensure that aviation finally pays for its full climate impact while funding the breakthrough technologies needed for a zero-emission future.

Recommendations

-

1

Expand the EU ETS to cover all departing flights from 2027, instead of continuing to rely on CORSIA.

-

2

Upgrade the Hydrogen Bank into a European-wide double sided auction mechanism to boost the uptake of e-SAF. Allocate e.g. 25% of aviation ETS revenues to the market intermediary.

-

3

Reform the SAF allowances in order to better support e-SAF by extending the mechanism in time and amount; earmarking allowances for e-SAF and advanced biofuels; phasing out support for HEFA-SAF; reducing the price coverage of the different types of fuels; and by moving away from an ex-post allocation to an ex-ante system.

-

4

Introduce an incentive scheme for airlines called contrail allowances using ETS revenues, to support airlines to perform contrail avoidance manoeuvres.

Part 1

Introduction

European aviation emissions surpassed their 2019 levels in 2025 for the first time since the pandemic, driven almost entirely by low-cost carrier growth. European aviation is recovering faster than any other part of the world, yet 68% of its emissions remain unpriced. With the EU's carbon market review due in 2026, the window to act is narrow.

European aviation has completely recovered from COVID

Methodological note: Throughout this report, we analyse emissions from all flights departing from European airports, covering the EU Member States, Norway, Iceland, Switzerland and the United Kingdom, referred to collectively as EU31. All figures refer to departing or outbound flights only, consistent with how emissions are reported and priced under the EU, Swiss and UK carbon markets.

European aviation emissions hits new emissions high in 2025

European aviation has crossed a symbolic threshold. According to Eurocontrol data, in 2025, flights departing from European airports generated 195 Mt of CO₂, returning to and surpassing their 2019 pre-pandemic level for the first time (192 Mt of CO₂ in 2019). Across 8.6 million departures, emissions rose 4% compared to 2024. This milestone is not cause for celebration. It confirms that the sector has rebuilt without cleaning up.

Aviation emissions have risen by more than 30% since 2005, moving in the opposite direction to virtually every other sector of the economy, making it the EU's fastest-growing source of emissions in the last 20 years.

The scale of this divergence is striking: in seven European countries, aviation has overtaken cars as a source of CO₂ and non-CO₂ emissions, despite carrying a fraction of the passengers.

A global picture: Europe leads the regional recovery

Flights departing from Europe accounted for more than 23% of worldwide aviation emissions, making it the third-largest emitting region after Asia (31%) and North America (25%). Despite its smaller share compared to the first two markets, Europe is the closest of these three regions to its pre-pandemic level.

We estimate that the two larger emitting regions are recovering more slowly: Asia remains 6% below its 2019 levels and North America, whose emissions declined in 2025 compared to 2024, falls 5% short of its pre-pandemic baseline.

At the country level, the United States and China together account for nearly one third of global aviation emissions, yet both recorded a 2% decline in 2025 compared to 2024 and remain below their 2019 levels.

The situation in European countries is more heterogeneous. The United Kingdom, Germany, Spain, France and Italy together represent around 12% of global aviation emissions - for comparison, this is roughly the same level as China - but their trajectories diverge substantially. Spain and Italy have already surpassed their pre-pandemic emissions, at 14% and 10% above 2019 respectively, driven by strong tourism recovery and growing low-cost capacity. Germany is the notable outlier among major European markets, still 16% below its 2019 level.

The policy response has not kept pace with the sector's growth

These figures contradict the pledges made by the aviation sector that it would build back greener after the pandemic. In T&E’s Down to Earth report, we estimated that passenger traffic at European airports could more than double by 2050. Fleet modernisation and sustainable aviation fuels have a role to play to reduce aviation emissions, but compliance with the EU's mandate on these fuels will not be enough to address the sector's continued growth. If Europe continues down this path, aviation could be burning as much fossil kerosene in 2049 as it did in 2023, even while complying with the EU's sustainable fuel mandate.

A robust market measure is the missing piece. This makes the upcoming 2026 review of the ETS for aviation particularly significant. Since 2012, the ETS has been limited to intra-EEA flights. A central question for this revision is whether it should be extended to all flights departing the EEA.

T&E analysis, outlined in this report, points to one conclusion: the urgent need to extend the scope of the ETS to all departing flights.

Part 2

Analysis

European aviation emissions have returned to pre-pandemic levels, yet the ETS leaves two-thirds of this pollution unpriced. By excluding long-haul flights and maintaining free allowances, airlines avoided an estimated €8.5 billion in emissions costs in 2025. Extending the scheme to all departing flights would close this loophole, align the sector with the polluter pays principle and unlock crucial revenues for the green transition of the sector.

Key figures on European aviation emissions pricing in 2025

The aviation carbon market remains a flawed system

European aviation has never polluted this much: the sector emitted 195 Mt of CO₂ from departing flights in 2025, exceeding its 2019 levels for the first time since the pandemic (+2% compared to pre-COVID levels).

The ETS has covered intra-EEA flights since 2012, with UK-to-EU routes switching to the UK ETS in 2021 following Brexit. Under both systems, airlines surrender allowances equal to their prior-year CO₂ emissions, acquired through annual allocations, auctions or secondary purchases, under a cap that tightens progressively over time.

In principle, a rising carbon price creates an incentive to cut emissions when doing so costs less than purchasing permits. In practice, the aviation cap is set separately from the rest of the carbon market and is already well below the sector's actual verified emissions. This means airlines must purchase general allowances, the same permits used by power stations and heavy industry, to cover the gap.

This dynamic is set to intensify in the future as the aviation cap reduces linearly and aviation emissions continue to grow, the gap between the aviation cap and actual (verified) emissions will likely increase. The relative importance of general allowances in airlines' compliance strategies is therefore going to rise significantly over the coming years. Put simply, airlines will need to purchase an increasing volume of general allowances to remain compliant, making aviation an ever-larger buyer in the broader carbon market.

A significant milestone in 2025 was the near-completion of the free allowance phase-out. Free allowances were reduced by 25% in 2024, by 50% in 2025 and will be fully phased out from 2026. In the UK, the phase-out follows a similar timeline. This has had a more substantial effect on the effective carbon price than the tightening of the cap itself: by reducing the volume of permits airlines receive for free, the phase-out directly increases the share of emissions that must be purchased at market price.

As a result, the estimated effective price per tonne of CO₂, meaning the price paid once free allowances and unpriced emissions are accounted for, rose to €22.6 in 2025. This is an increase of 26% compared to last year’s estimate of €17.9. For comparison, in the same period the average allowance prices under the general ETS increased by 13% and UK-ETS increased by 29%, due to the tightening cap.

The more fundamental shortcoming of the aviation ETS remains scope. The European carbon markets covered 74 Mt of CO₂ in 2025 (considering emissions from EU and Swiss administered airlines, plus UK ETS estimated emissions). Had they applied to all departing flights, a further 107 Mt would have been included. Taking unpriced international emissions and remaining free allowances together, 68% of CO₂ from European departing flights went unpriced in 2025.

The breakdown is unequivocal. Intra-European emissions have grown 4.5% in 2025 and now are 11% above their 2019 level, the strongest recovery of any segment. Extra-European emissions, which the ETS does not price, grew 3% in 2025 but remain nearly 6% below their pre-pandemic levels. The segment growing fastest and furthest above 2019 is the one the system already prices, yet emissions have continued to rise. Both a broader scope and a more ambitious carbon price are needed.

The most polluting routes: long-haul escapes pricing, short-haul misses the train

Long-haul routes continue to escape carbon pricing entirely. None of the most polluting routes departing from Europe in 2025 fall within the scope of the current ETS schemes. Every flight in the top ten ranking is intercontinental and therefore exempt from EU, Swiss and UK carbon pricing alike.

London-New York remains the single most polluting departure route, generating nearly 1.4 Mt of CO₂ in 2025 (all departing flights combined), roughly equivalent to the annual emissions from all combustion cars in a city the size of Munich. Most of the other top-ranked routes depart from London, reflecting the scale of long-haul traffic through UK airports (especially London Heathrow). The highest-ranked EEA-originating route is Frankfurt-Shanghai, in fifth place, with 0.7 Mt of CO₂. To find the first route covered by the current ETS, one must scroll to the 131st place: London-Milan, which falls under the UK ETS, with 0.16 Mt of CO₂ in 2025.

This highlights the key loophole in the European carbon pricing system: the flights doing the most damage are precisely those the system does not reach.

Closer to home: Europe's most polluting short-haul routes have a rail alternative. Due to the current ETS scope, intra-European routes are already priced. However, pricing alone is only part of the picture. Many of the most polluting short-haul routes within Europe connect city pairs where a credible rail alternative exists. These are routes where carbon pricing, combined with the right conditions for modal shift, could deliver the most immediate emissions benefit.

Looking specifically at routes where a rail journey can be completed within 8 hours, several of Europe's most polluting intra-European departures stand out. London-Amsterdam can be reached in around four hours by rail. London-Edinburgh takes roughly four hours. Paris-Barcelona is under seven hours, and both Milan-Paris and Geneva-London can be completed in approximately seven hours. Together, these routes generated 0.5 Mt of CO₂ in departing flights alone or 1 Mt when both departing and arriving flights are counted.

To put this in perspective, this is less than the emissions of a single route in the previous, global ranking: the kind of figure generated by the yearly departing emissions of the London-Dubai or London-Singapore routes alone.

London-Milan remains the most polluting intra-European route overall, generating 0.16 Mt of CO₂ from departing flights in 2025 (roughly 9 times less than London-New York). That it is simultaneously one of the most polluting short-haul routes and one with a clear rail alternative (rail equivalent journey can be done in two legs), underlying how much the current policy framework leaves on the table.

That so many of Europe's most polluting short-haul routes already have a rail option makes the barriers to using it all the more frustrating. For many passengers, the will to travel by train exists, but the conditions do not. On cross-border routes in particular, train fares frequently exceed the cost of flying by a significant margin, direct connections aren’t always possible and booking a through-ticket across multiple operators can be a near-impossible task. A recent T&E survey, conducted with YouGov, found that 61% of rail passengers had already avoided booking a rail journey because the booking process was too complicated. The result is that passengers are pushed towards the most climate-damaging option not by preference, but by a system that has failed to make the sustainable choice the easy one.

A more recent T&E study found that on half of the most flown routes within the EU, booking a rail equivalent journey from dominant rail operators is complicated or impossible. Carbon pricing creates a financial incentive to shift demand, but it works most effectively where a competitive alternative is not only available but also easy to book. For the routes identified here, the alternative is available. What is missing is a high enough carbon price and a reliable, affordable and easy-to-use rail network to make the choice straightforward for passengers.

Airlines under the carbon market: growing fast, paying little

Aviation is the only major emitting sector in Europe that does not fully pay for its pollution. While industry, power generation and other heavy emitters face a progressively tightening carbon price across their full output, aviation benefits from a combination of scope exemptions and free allowances that leave the majority of its emissions unpriced. The gap has widened as the sector has grown.

Low-cost carriers drive European emissions growth

At the airline level, growth has been concentrated among low-cost carriers. Ryanair remains Europe's most polluting airline, emitting 16.6 Mt of CO₂ from departing flights in 2025, roughly equivalent to the total annual CO₂ emissions of a country the size of Croatia. This is a 3% increase compared to 2024 and approximately 1.4 times its 2019 level. The top ten most polluting airlines together accounted for 41% of all emissions from European departing flights, a share that has remained broadly stable in recent years.

The divergence is even more pronounced when looking beyond Europe. Among the world's 20 highest-emitting airlines globally, Ryanair recorded the largest emissions increase of any airline worldwide since 2019, with emissions now 50% above its pre-pandemic level. European legacy carriers tell the opposite story: Deutsche Lufthansa AG, British Airways and Air France are all still below their 2019 levels, broadly in line with legacy peers from other parts of the world.

Put simply, low-cost expansion, not legacy recovery, is what is pushing European emissions back towards and beyond their pre-pandemic peak.

How little airlines are paying

Low-cost carriers, whose networks are concentrated within Europe, pay for a higher share of their emissions simply because more of their flights fall within the ETS scope. Legacy carriers, with large long-haul networks, pay for far less. Non-European carriers pay the least of all.

The chart below shows the effective price paid per tonne of CO₂ by the ten highest-emitting airlines in 2025, considering the average EU, Swiss and UK ETS prices of €73 and £48 (€55), free allocations and scope exemptions.

In total, airlines operating in Europe paid nearly €4.1 billion for EU, Swiss and UK ETS allowances in 2025. An estimated €8.5 billion in emissions costs went unpaid, a consequence of remaining free allowances and, more importantly, the exclusion of long-haul flights.

Low-cost carriers paid for a higher share of their emissions given their Europe-focused networks. Even so, the gap remains visible: Ryanair, easyJet and Wizz Air left 26%, 24% and 35% of their emissions costs unpaid in 2025 respectively. This is primarily because free allowances, while sharply reduced, had not yet been fully eliminated in 2025. Meaning that even on routes covered by the carbon market, a portion of emissions were not subject to a charge.

Legacy carriers such as Deutsche Lufthansa AG, British Airways and Air France left 72%, 78% and 82% of their emissions costs unpaid in 2025. This is largely explained by the high share of long-haul flights in their networks, falling outside of ETS coverage. Non-European carriers, including Emirates and United Airlines, emit at comparable levels to their European peers overall yet pay even less, if not zero, as virtually all their flights are international. This is a competitive distortion. Extending the carbon market to all departing flights would bring non-European airlines into scope and align the system with the polluter pays principle.

Based on these numbers, we can conclude that European ETSs currently add just €7 to the cost of an intra-EU31 flight ticket on average. Passengers on international routes pay nothing, as the scheme does not yet cover flights outside the EU. If the ETS were extended to all departing flights from EU31, the average additional cost for a passenger travelling outside the EU would be €45 per ticket. Across all departing passengers, the average cost would remain under €17 per ticket.

These figures deserve context. A recent T&E analysis shows that for long-haul flights, the current geopolitical oil shock of the Iran crisis is adding around €90 per passenger to fuel costs, while the SAF mandate adds around €3. The carbon market adds nothing, as it does not apply to long-haul routes. Extending the ETS to long-haul flights would add roughly half of what passengers are paying today because of fossil fuel price volatility.

The same can be said about short-haul flights. Fossil fuel volatility adds around €30 to fuel costs, while all climate policies combined (current ETS and RefuelEU compliance) add less than €10.

Ticket prices are rising because of Europe's dependence on fossil fuels, not because of the measures intended to steer the sector away from them.

Extending the carbon market to all departing flights could unlock billions in additional revenue

As mentioned before, airlines operating in Europe paid €4.1 billion in 2025 under the ETS aviation, covering just 32% of departing emissions. Had the schemes applied to all departing flights, revenues could have reached nearly €12.7 billion under the same carbon price conditions, unlocking an additional €8.5 billion for public budgets to direct towards the green transition. Two main schemes using ETS revenues for aviation decarbonisation stand out: the SAF allowances and the Innovation Fund. Part 3 of this report also explores how carbon pricing can spur the use of greener aircraft, namely electric and hydrogen planes.

The main beneficiaries of a scope extension would be Member States themselves. With the current rules, we estimate that Member States will receive roughly €3 billion from auction revenues (about 72% of the total €4.1 billion paid by the airlines), given that part of the allowances are non-auctioned or used for the Innovation Fund and other schemes.

If the scope had been extended in 2025, it would have brought €7.5 billion to national budgets (assuming that the additional allowances were purchased from the general ETS cap). Countries with large aviation sectors already capture the largest shares: Germany, Spain, Italy, Poland and France rank among the top recipients under the current scope.

Looking ahead, with a full scope extension to all EU31 departing flights, total revenues could reach more than €17 billion a year by 2030, driven by market growth and the completion of the free allowance phase-out from 2026.

Some Member States would gain disproportionately. Poland, for instance, would become the second-largest beneficiary of carbon market revenues from aviation, alongside substantial gains for Czechia, Romania and Greece. This reflects the way general allowance auction shares are allocated: based on historical industrial emissions rather than aviation activity, countries like Poland and Czechia hold higher shares that translate into outsized gains when airlines increase their demand for allowances through a scope extension.

These revenues represent a significant and growing public climate fund. The European Commission's upcoming revision of the carbon market offers a direct opportunity to transform it into a leading policy instrument for aviation decarbonisation, above all by scaling up sustainable aviation fuel production and incentivising contrail avoidance. As outlined previously, T&E recommends that approximately 25% of ETS aviation revenues should be repurposed for the greening of the sector, through three measures:

-

Reform of the Hydrogen Bank into a market intermediary for e-SAF: T&E recommends earmarking a share of ETS aviation revenues to transform the Hydrogen Bank into a market intermediary for e-fuels. This entity would conduct double-sided auctions, signing long-term purchase contracts with producers to ensure bankability and reselling to airlines via shorter-term contracts to manage price risk. This structure, which can be implemented under the existing ETS framework by 2027, would bridge the price gap, provide transparent market signals and de-risk the transition to e-fuels.

-

Redesign of the SAF allowances to better unlock e-SAF investment: To move beyond the current ex-post, "first-come-first-served" system - which largely subsidises HEFA-SAF and expires in 2030 - T&E calls for an extension of the mechanism to 2034 with an increased pool of 30 million allowances. This reform should prioritise scalability by earmarking 50% of support for e-SAF from 2030, phasing out HEFA subsidies and shifting to an ex-ante allocation model. By allowing airlines to secure support based on binding forward offtake agreements rather than annual claims, the system would provide the long-term revenue certainty necessary for e-SAF projects to reach final investment decisions and meet EU sub-mandates.

-

Establish a contrail allowance scheme: To address aviation’s non-CO2 climate impact, T&E proposes using 1.5% of current ETS aviation revenues (approx. €50 million annually) to fund a "world-first" incentive scheme for contrail avoidance. This mechanism would cover the marginal fuel and operational costs via CAPEX allowances for integrating forecast technology and OPEX allowances to cover additional fuel burn. By incentivizing the systematic redirection of flights to avoid warming contrails, the EU could achieve a climate benefit of 20–40 million tonnes of CO2 equivalent annually without placing a significant financial burden on the industry.

CORSIA is not a credible alternative to the European carbon market

The contrast between the EU’s cap-and-trade system and CORSIA, ICAO's global offsetting scheme for international aviation, is stark.

Our analysis finds that CORSIA would cost European aviation between €7 billion and €43 billion over the next ten years, a wide range reflecting deep uncertainty about credit supply and participation. None of that money would stay in Europe. It would instead flow to global offset providers, with no guarantee of genuine emissions reductions and little transparency over how payments reach the local communities the credits are supposed to benefit.

CORSIA credits still remain far cheaper than ETS allowances, which means they provide no meaningful price signal for decarbonisation. A cap-and-trade system sets a hard limit on emissions and makes polluters pay progressively more as the cap tightens. CORSIA does neither.

The case for keeping the EU ETS in its current, limited scope has long rested on the existence of CORSIA. Through three successive stop-the-clock derogations, the latest running until 2027, the EU has exempted all flights to and from the EEA from carbon pricing, on the assumption that CORSIA provides an equivalent safeguard. Our analysis shows it does not. The EU has committed to evaluating whether CORSIA delivers emissions reductions in line with its climate goals and the Paris Agreement by 1 July 2026. If CORSIA is deemed insufficiently robust, meaning ICAO has not strengthened the scheme in line with achieving these goals and fewer than 70% of international aviation emissions are covered, the European Commission could propose to apply the ETS to all departing flights from 2027. Our analysis shows that such a conclusion is inevitable.

The scheme's coverage is structurally limited. CORSIA applies only to international flights between participating states, leaving domestic aviation entirely outside its scope. Participation, meanwhile, is more fragile than headline figures suggest. Key aviation markets including China, Brazil, Russia, India and the United States have not implemented CORSIA into national law. Based on 2022 analysis, participating states account for 66% of global aviation emissions, a share that could fall further if non-implementing countries withdraw.

Even within its scope, CORSIA addresses only a fraction of the problem. Airlines must offset emissions above a baseline set at 85% of 2019 levels. Our analysis finds that, on this basis, just 26% of EU aviation's CO₂ emissions will be covered by the scheme by 2035. There is no cap, no emissions reduction built into the design and no enforcement power at ICAO level in the event of non-compliance. Airlines can continue to grow their emissions indefinitely, provided they purchase sufficient offsets.

In 2025, European airlines left €8.5 billion in emissions costs unpaid. Every year the carbon market fails to cover all departing flights is another year the aviation industry passes that cost to society.

The quality of those offsets is itself a serious concern, even as more projects are technically entering the market. A recent analysis revealed that, while the pool of eligible credits reached 32 million units by early 2026, including new clean cooking projects from Africa, the Guyana ART TREES programme still accounts for 90% of recent issuances. Analysis of this programme found that 84% of its credits resulted from an artificial adjustment for countries with low deforestation rates, a practice the UN review team found does not represent genuine emissions reductions. Furthermore, host country approval remains a significant bottleneck to high-quality supply; for instance, a major clean energy project in Kenya recently collapsed after failing to secure the necessary government authorisation. This reinforces that the scheme relies on a fragile and often low-quality supply chain that cannot guarantee the climate integrity required by the EU.

Beyond environmental integrity, there are also unresolved questions about who benefits financially from credit sales. Research by Carbon Market Watch found a persistent lack of public data on how payments are distributed between intermediaries, project developers and the local communities nominally at the centre of these projects. An investigation into BP's use of credits from rural Mexico found that local communities received only a fraction of the market price, with intermediaries capturing the remainder. This is not an isolated case: the companies that own and manage offsetting programmes are overwhelmingly based in high-income countries, while the projects themselves are concentrated in lower-income ones. The result is a scheme that risks transferring billions of euros out of Europe in exchange for offsets that deliver little for the climate and even less for the communities they claim to support.

The conclusion is clear. CORSIA is not a credible substitute for extending the European carbon markets to all departing flights. It covers too few emissions, enforces too weakly and relies on credits whose environmental integrity cannot be assured. The EU's assessment of CORSIA's robustness should reflect this reality.

It is important to note that extending the ETS to all departing flights would not require dismantling CORSIA. The two systems can coexist. Under Article 28b of the ETS directive, airlines are not required to pay twice for the same emissions: where a flight is covered by both the ETS and CORSIA, ETS takes precedence and the CORSIA obligation is deducted accordingly. We estimate that CORSIA offsetting requirements for flights within the EU31 amounted to 10.6 Mt of CO₂ in 2025, at a cost of around €146 million at current credit prices. This figure would be fully offset against ETS compliance obligations. A scope extension from 2027 would expand this deduction mechanism to a larger share of international routes, but the underlying principle remains the same. Airlines would face one carbon price, not two. The case for extending the carbon market is not a case for replacing CORSIA, it is a case for ensuring that European aviation finally pays for the full cost of its emissions, on every route it flies.

Part 3

Ending aviation tax exemptions will unlock investments in revolutionary planes, including hydrogen and electric aircraft

Aviation is the only major industry that has never paid for the fuel it burns. No fuel tax, no VAT on international tickets and no meaningful carbon price on long-haul flights. Decades of these exemptions have done more than cost public budgets billions in foregone revenue. They have removed the single most powerful incentive for aircraft manufacturers to innovate: the prospect that cheaper, cleaner technology will outcompete a dirty one.

The consequences are visible in the industry’s own product pipeline. The commercial aircraft market is dominated by a duopoly, Airbus and Boeing, which severely limits competition and disincentivises the creation of disruptive aircraft. Neither manufacturer has introduced a clean-sheet aircraft design since 2015. Instead, both have spent the intervening decade fitting new engines onto airframes designed in the 1960s and 1980s.

Our previous analysis found that no new aircraft models are expected from either manufacturer in the next ten years, leaving the European fleet locked into a stalled efficiency trajectory for at least another decade. With fossil jet fuel kept artificially cheap, there is simply no commercial case for the multi-billion-euro investment that a genuinely new aircraft requires. The market signal that should be driving that investment, namely the rising cost of polluting, has been deliberately suppressed.

The fragility of this model was exposed by the 2022 oil price shock, a stark warning that the industry largely ignored, making the current 2026 crisis an inevitable consequence of a system built on artificially cheap energy. An aviation ecosystem built around the assumption of cheap, untaxed fossil energy is not a resilient one. It is a system that has traded long-run decarbonisation capacity for short-run cost comfort and it will remain exposed to exactly these shocks for as long as manufacturers have no incentive to develop aircraft that use less of it.

Extending the EU carbon market to all departing flights changes this calculus. A meaningful and rising carbon price raises the operating cost of fossil-fuelled aircraft year after year, while simultaneously narrowing the price gap between today’s polluting planes and more efficient planes, including zero-emission hydrogen and electric aircraft, that are technically feasible but commercially stranded.

We quantified this effect. Using a total cost of ownership model, we compared two scenarios: one in which the carbon market continues to apply only to intra-European flights and one in which it extends to full scope, covering all departing flights from 2027. The model tracks the full economics of aircraft development and operation across regional, single-aisle and widebody aircraft classes covering both revolutionary next-generation kerosene aircraft and zero-emission hydrogen and electric alternatives, from entry into service through to fleet retirement. It incorporates manufacturer development costs, airline fuel and carbon expenditure and projected SAF blending mandates under ReFuelEU.

Our central estimate is that an additional carbon price of €121 per tonne of CO₂ would be sufficient to make cleaner aircraft cost-competitive with conventional alternatives at a system level. Crucially, this figure sits within the range of carbon prices that current EU ETS projections already imply by the mid-2030s. The policy lever needed to tip the economics is not out of reach.

However, if the ETS scope is not extended after 2027, the additional carbon price needed to make efficient technologies cost competitive rises to €245 per tonne of CO2. Restricting the scope of the ETS would hinder the economic case for new aircraft, incentivising the aviation industry to stick to a logic of low cost, incremental improvements which has slowed down technological progress in recent decades.

That support requirement is visible in the numbers. Bringing revolutionary aircraft to market would require an estimated €186 billion in development expenditure across all manufacturers, compared to €26 billion in a scenario where only conventional next-generation aircraft are built. This seven-fold difference in upfront capital is the core structural barrier. It is also precisely the gap that revenues from a fully scoped carbon market could help to address: through industrial support measures like the Innovation Fund, the Clean Aviation Joint Undertaking successor programme and measures to bring the cost of capital down for the development of revolutionary aircraft technologies.

The benefits add up for operators. Over the model horizon, airlines flying next-generation aircraft face structurally lower exposure to fuel price volatility. In the scenario, operators spend nearly €800 billion less on fuel than if they continued to fly conventional aircraft. This saving materialises precisely when energy prices are high or volatile and therefore when the conventional fleet is most exposed.

This would obviously translate into an emissions benefit. In the scenario with more efficient aircraft, airlines emit approximately 380 Mt fewer cumulative CO₂ emissions over the period, roughly equivalent to the total annual CO₂ emissions of a country the size of Australia. In a world of adequate carbon prices or repeated oil price shocks, zero-emission aircraft are not just cleaner. They are cheaper to operate. The carbon market, in other words, does not simply penalise the business-as-usual. It makes the alternative worth building, while providing a predictable price signal to help the financial planning of operators, unlike oil price shocks.

Part 4

The importance of non-CO₂ emissions and the need to address aviation’s full climate impact

The EU’s Monitoring, Reporting and Verification (MRV) framework for non-CO₂ aviation effects is a critical step toward addressing aviation’s full climate impact. But currently, its limited scope fails to capture the full extent of aviation’s non-CO2 effects. It must be maintained and expanded as a “no-regret” instrument that builds the evidence base, enables future regulation and supports near-term mitigation.

There is a broad scientific consensus that aviation’s non-CO₂ effects are of a similar order of magnitude to its CO₂ impact. It is therefore crucial to consider these emissions in European climate policy. An important step in the right direction was the launch of the Monitoring, Reporting and Verification (MRV) scheme of aviation’s non-CO₂ emissions in January 2025. The system enables the collection of data on non-CO₂ effects. Although co-legislators agreed that the MRV would cover all flights from and into the EEA area, airline lobbying restricted its application for the first two years to intra-EEA flights only. As of 1 January 2027, the scope will be automatically extended to all flights arriving to or departing from the EEA. By the end of 2027, the Commission will assess the MRV data and, if appropriate, propose legislation to address these effects.

The non-CO₂ emissions reported by airlines for the year 2025 will only be available later this year due to a delay of reporting. Therefore, we give an estimate of the share of European aviation’s contrail warming not captured by the reduced scope MRV based on our own analysis of 2025 data, as well as an overview of the most polluting flight destination countries. We find that the reduced intra-EEA scope in the first two years leaves more than 50% of European contrail warming outside the scheme. Maintaining the extension of the scheme to all EEA flights therefore matters not just for accuracy, but for credibility. If the major warming effects are on long-haul flights and those flights are left out, the evidence base for future policy will be incomplete.

Part 5

Recommendations

-

1

Expand the EU ETS to cover all departing flights from 2027, instead of continuing to rely on CORSIA. The European carbon markets covered 74 Mt of CO₂ in 2025. Had it applied to all departing flights, a further 107 Mt of CO2 would have been included - generating an additional €8.5 billion in revenues.

-

2

Use the upcoming revision of the carbon market as an opportunity to transform it into a leading policy instrument for aviation decarbonisation, above all by scaling up sustainable aviation fuel production and incentivising contrail avoidance: 1) Upgrade the Hydrogen Bank into a European-wide double sided auction mechanism to boost the uptake of e-SAF. Allocate e.g. 25% of aviation ETS revenues to the market intermediary. 2) Reform the SAF allowances in order to better support e-SAF by extending the mechanism in time and amount; earmarking allowances for e-SAF and advanced biofuels; phasing out support for HEFA-SAF; reducing the price coverage of the different types of fuels; and by moving away from an ex-post allocation to an ex-ante system. 3) Introduce an incentive scheme for airlines called contrail allowances using ETS revenues, to support airlines to perform contrail avoidance manoeuvres.

-

3

Consider additional decarbonisation measures - such as short-haul flight bans under Article 20 of the Air Services Regulation - to address top-polluting intra-European aviation routes.

-

4

Maintain and strengthen Innovation Fund support to European innovative companies developing disruptive aviation technologies, including electric, hybrid and hydrogen aircraft.

-

5

Automatically expand the scope of the non-CO2 MRV to cover departing and incoming flights, to better the understanding of aviation’s full climate impact

Related Articles

View All

Press Release

EU takes half-hearted step towards taxing international flights

Extension of ETS to some international flights, private jets and to smaller ships are steps forward, but overall weakening of the ETS undermines Europ...

Opinion

The climate deal Trump won’t kill

Press Release

Booming air tourism could fuel European rent hikes of up to €250 a year

Southern Europe and Ireland hit hardest by air tourism-driven housing crisis, T&E study finds