The presence of Chinese automakers in the EU car market

Analysis of the impact of EU tariffs on BEV imports from China.

Authors

Ludovico Machet

Analyst InternExecutive summary

Key finding: The EU’s EVs tariffs worked but will not stem the rise of Chinese EV sales into the EU.

The ‘positive’ impact of the EU’s EV tariffs:

-

Made-in-China cars dropped to 17% of BEV sales (Q1 2026, EU) down from a peak of 22% in 2024 (activation of EV tariffs). Volumes have stabilised around 350k units.

-

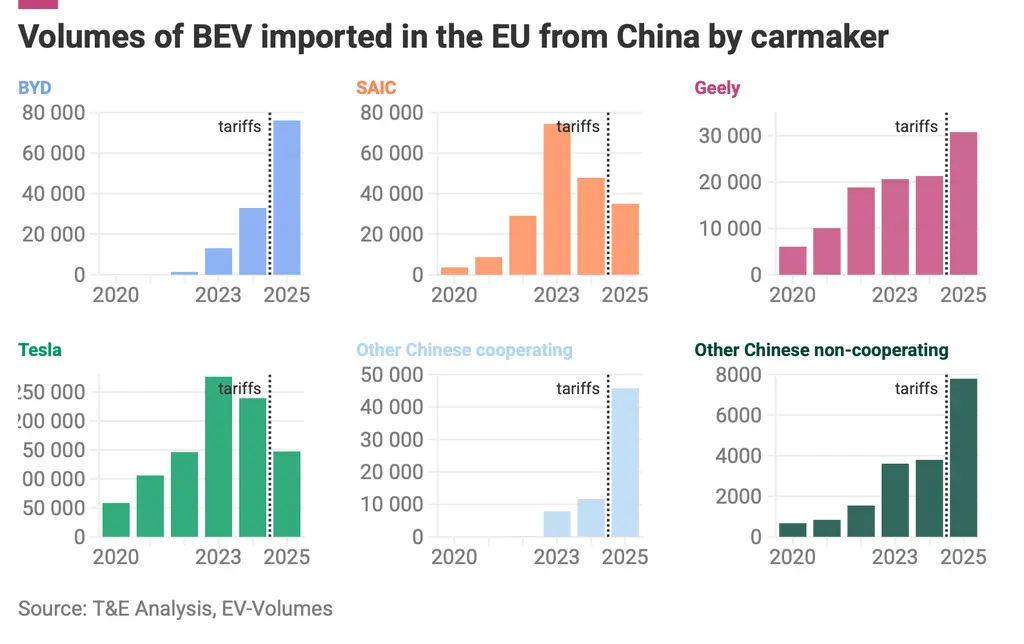

Chinese OEMs are responsive to tariffs but the EU’s different rates lead to different results. SAIC’s (35% tariff) sales into the EU nearly halved with respect to a 2023 peak. BYD’s (17%) sales more than doubled.

-

Western OEMs shifted production to Europe. European OEMs’ Made-in-China BEV imports dropped from 38% to 23% between 2024 and Q1 2026, while Tesla dropped from 26% to 19% over the same period (down from 55% in 2021)

-

Chinese OEMs are onshoring BEV production to Europe with production set to increase to 600k units in 2035. 10 planned production facilities have been announced since the EU Commission president opened the anti-subsidy investigation in September 2023.

Where the EV tariffs fell short:

-

Battery exports (exempt from tariffs) from China have increased seven fold from around $4bn in 2020 to nearly $30bn in 2025.

-

Chinese EVs remain 21% cheaper on average and Chinese OEMs’ share of cars shipped from China to Europe has risen from 35% to 54% (offsetting lower European and Tesla imports).

-

Made-in China PHEVs (exempt from tariffs) rose from 37% (2024) to 60% (2026) of total PHEV imports into the EU.

-

Despite onshoring, Made-in-China BEVs are expected to account for 60% of Chinese brand sales in Europe, rising from 350k units in 2025 to 850k by 2035.

-

Chinese onshoring is heavily focused on 3 countries: Turkey, Hungary and Spain.

-

Chinese-brand BEV could displace ~10 legacy car factories.

-

Lower BEV sales by EU carmakers co-determine China’s BEV market share in the EU. Weaker EV targets (in line with the proposals discussed in the EU Parliament) would increase the market share of Chinese carmakers from 15% to 30% of BEVs in 2035 (with a majority being Made-in-China).

Key data

Breakdown of findings

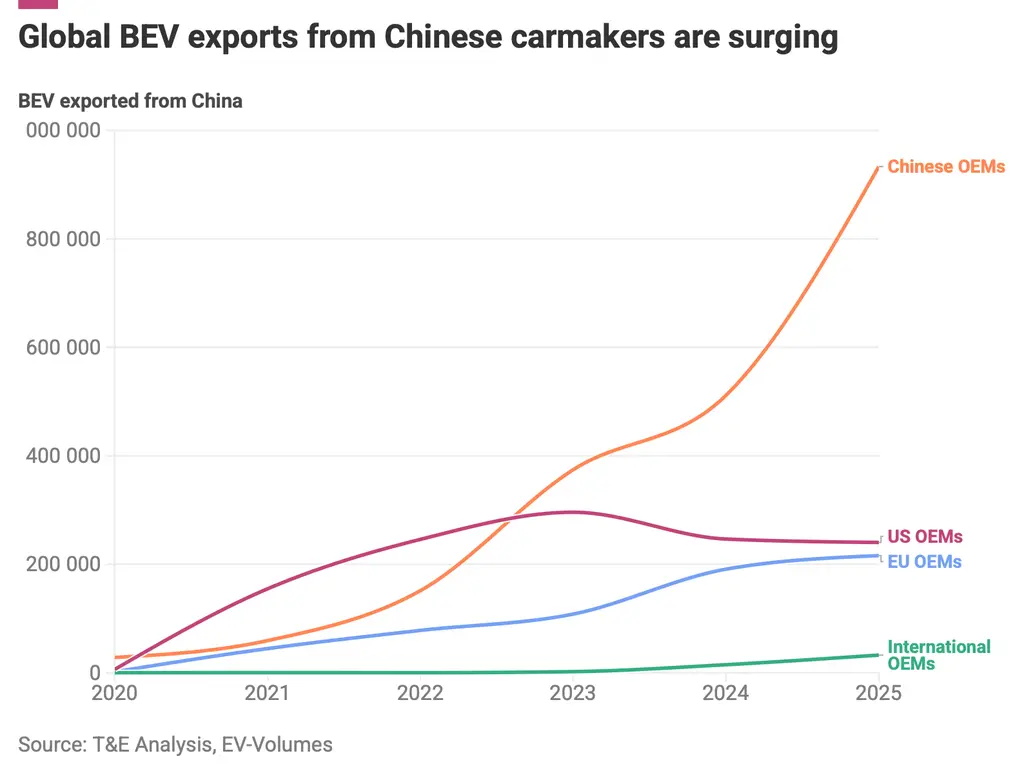

Exports from Chinese automakers have surged to 1m cars per year

Chinese OEMs are turning to exports to absorb overcapacity. Europe is a key export destination (30%, incl. 8% for the UK), second to Asia-Pacific.

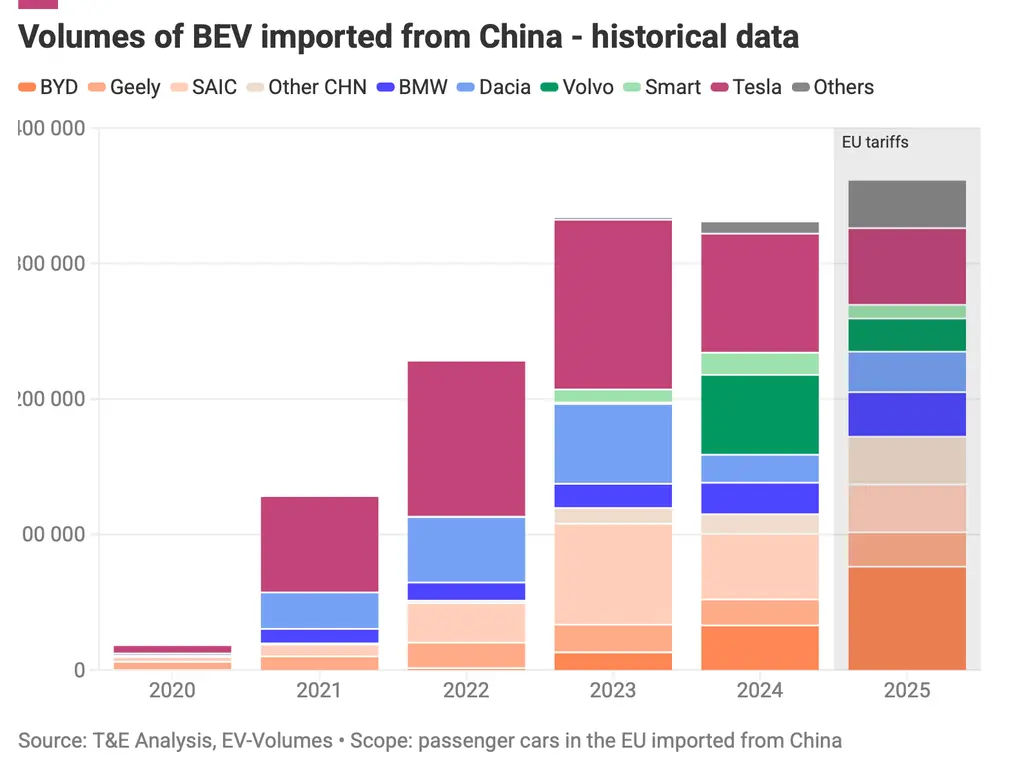

Imports of Made-in-China BEVs have stabilised at around 350k units

-

EV tariffs worked (for EU and US OEMs), but have not stemmed Chinese OEM’s overcapacity-driven exports.

-

Imports from China at 350k units in 2025, driven by an increase from BYD and Geely.

-

International brands such as Tesla, Volvo and Smart reduced their imports.

Chinese OEMs now account for more than half of BEV imports from China

-

Chinese OEMs now account for more than half of imports from China (from 15% in 2021).

-

Over the same period, Tesla’s share of imports dropped from 55% to 19% as they localised to Berlin (2022).

-

EU OEM imports dropped from 38% to 23% between 2024 and Q1 2026 (localisation of models like Volvo EX30).

Made-in-China BEVs now account for 17% of BEVs

-

The share of BEVs that are made-in-China BEVs peaked in 2024 with the activation of EU EV tariffs.

-

Growth of the EU BEV sales from 2025 (car CO2 targets), led to a contraction of the share of Made-in-China BEVs despite volume of imports from China growing in 2025.

-

SAIC, Tesla, Volvo and Smart (Other INT) reduced imports (and often onshored), while Chinese carmakers like BYD, Geely grew their share despite the growing market

Tariffs effect on Chinese carmakers: BYD vs SAIC

Lower tariffs (17%) for BYD allowed BEV sales to grow, while higher tariffs for SAIC (35%) led to a decrease.

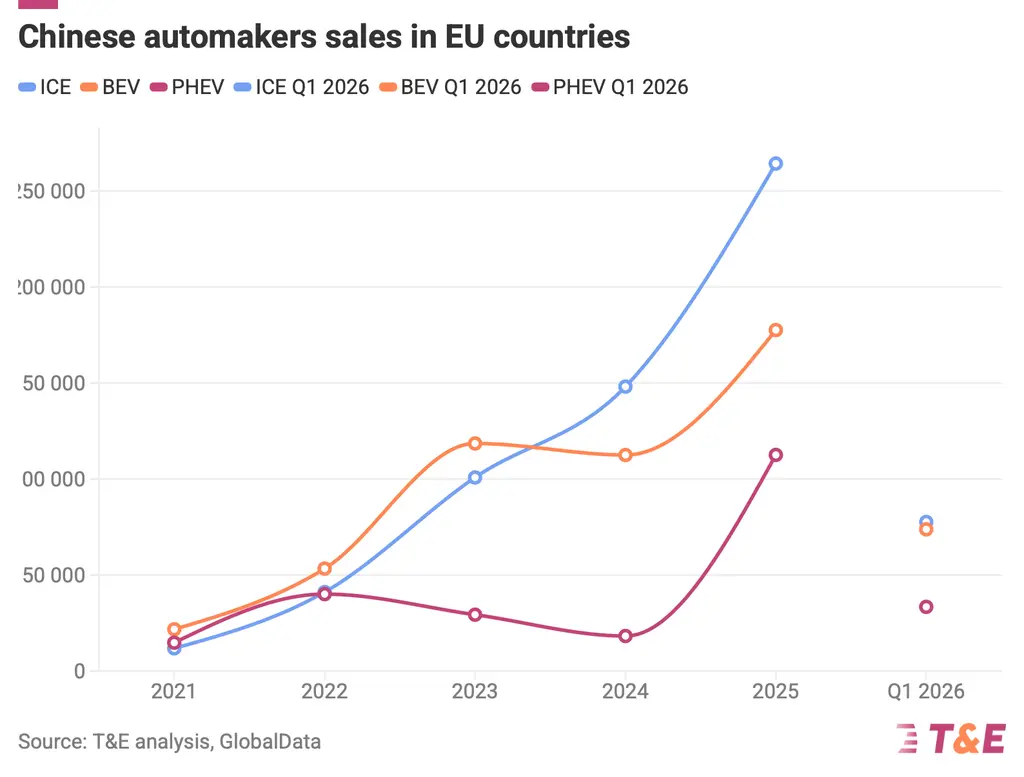

Total car sales from Chinese automakers grew to 550k units in 2025

550k cars sold in the EU by Chinese OEMs in 2025 (around half are ICEs). 97% of Chinese-brand ICEs are imports vs 97% for PHEVs and 99% for BEVs.

Weaker CO2 targets will cede the BEV market to Chinese carmakers

A weakening of the CO2 targets (in line with the proposal from the lead rapporteur in the European Parliament, M. Salini) would increase the market share of Chinese carmakers from 15% to 30% in 2035.

Imports account for ~60% of Chinese brand BEV sales in 2030-2035. As a result Chinese brand imports from China could rise to 17% of BEV sales if the targets are weakened or decrease to 8% if they are kept (from 9% today).

Chinese production in the EU - plants localisation

Chinese OEM are onshoring production - from 0 to 1m (mostly BEVs)

Chinese overcapacity demands stronger EU regulatory action and trade defense

Conclusion

The Chinese EV market has returned to growth despite reports of a sales collapse after the scrapping of Chinese EV subsidies early 2026. China’s rapid electrification continues, relying heavily on export markets to absorb significant domestic overcapacity. With the US market effectively closed, Europe represents a primary destination (second to the APAC region) where vehicles can be sold at higher profit margins.

While the 2024 BEV tariffs successfully drove the relocalisation of Western OEMs and the onshoring (or nearshoring in Turkey) of Chinese production, pressure remains acute. Rising imports of Chinese-manufactured BEVs, PHEVs, and ICE vehicles —fuelled by unprecedented overcapacity– threaten EU automaker employment, necessitating decisive policy intervention.

To address this, the EU must: 1) ensure European automakers remain on track and prioritise EV sales by safeguarding the ambition of EU car CO2 regulations; 2) establish robust final investment decision (FDI) rules for Chinese OEMs producing in Europe under the IAA; and 3) activate appropriate trade defence mechanisms.

Specifically, the EU must increase tariffs on Chinese battery imports. These duties remain exceptionally low (1–3%) despite the EV anti-subsidy investigation confirming that Chinese battery production is heavily subsidised. Without immediate action to support EU-based producers, the domestic battery industry may not survive.

Additional measures to be considered by the EU

-

1

Expand trade measures to batteries - increasing the tariff from its current ultra-low level to a level that would help EU based producers compete and encourage further Asian onshoring. From an economic security POV the EU should adopt a whole of value chain (CAM, pCAM) which it should phase in gradually.

-

2

Prevent circumvention of EU trade measures through moving manufacturing to non-EU countries with trade or customs deals with the EU.

-

3

Support the speedy adoption of the IAA and Corporate Fleets law to create a strong market for Made-in-EU EVs and batteries

-

4

Protect EU car electrification by safeguarding the car CO2 targets for 2030 and 2035.

Related Articles

View All

News

What the Electrification Action Plan means for transport

T&E's in-depth review of the EU Commission's Electrification Action Plan

Report

Europe’s waste creates value elsewhere

How the Circular Economy Act can provide the tools to help scale Europe’s recycling industry, in order to secure access to critical minerals.

Press Release

Charging infrastructure has far outpaced EV sales in all but one EU country – analysis

Only Malta falls short on the EU’s fleet-based target for public charging.