Europe’s automotive industry at a crossroads

A new study models the impact of EU electric vehicle leadership and ambitious policies on investment and jobs.

Summary

Making Europe’s EV industrial leadership a priority

Downloads

Lead authors

The automotive industry and its supply chain are undergoing an unprecedented industrial transformation from vehicles running on combustion engines to electric cars powered by batteries, motors and chargers. The global competition to onshore these clean technologies is immense, and Europe’s success hinges on the market and industrial policies adopted today.

This new research by T&E shows that Europe must urgently establish global electric car leadership to sustain economic value and create new jobs across its automotive value chain and surrounding industries, such as batteries and charging.

Among the three possible scenarios designed for this study, Europe’s best possibility to maintain the economic contribution of its automotive value chain requires keeping the integrity of its 2035 CO2 zero-emission car goal, combined with strengthened industrial and demand policies to make local manufacturing attractive and accelerate electric vehicle uptake.

This package of actions can - if comprehensively delivered and all other things being equal:

-

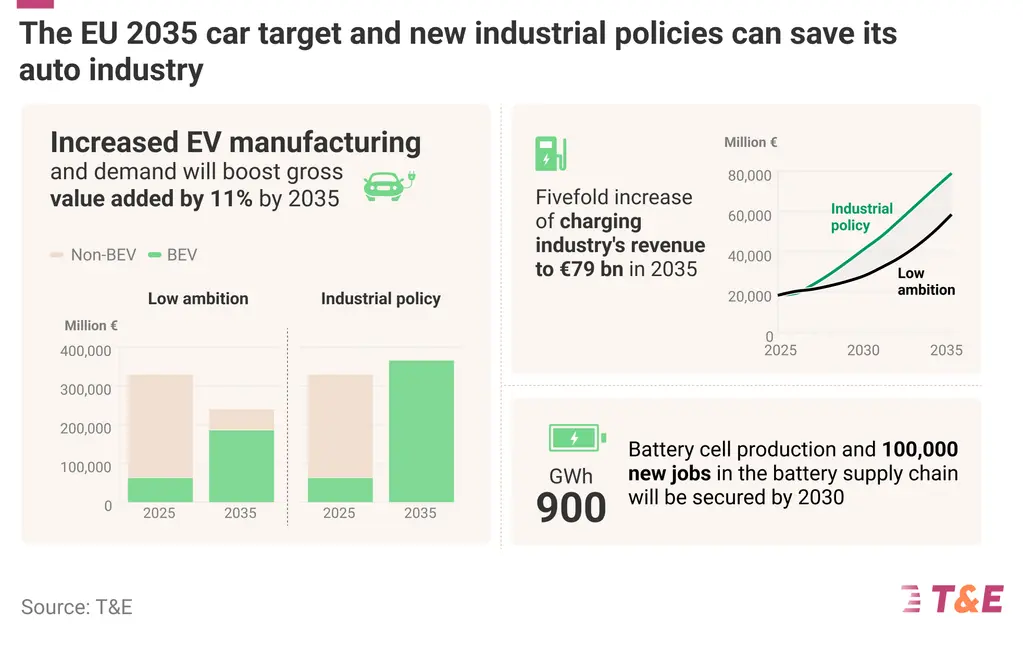

Help recover car production levels thanks to increased EV manufacturing and demand, reaching 15.2 million units by 2030 and 16.8 million by 2035. This would translate into keeping the current automotive job levels in the next decade.

-

Secure over 900 GWh of battery manufacturing and over 100,000 new jobs in the sector by the end of the decade, flanked by a growing cathode active material industry and lithium refining in Europe.

-

Increase the charging industry’s economic output almost fivefold to €79 billion, creating 120,000 jobs by 2035.

Walking back from 2035 and no industrial policy risks leading to automotive industrial decline

The scenario where the EU walks back from its 2035 goal and fails to deliver adequate industrial policy action would see the strongest decline in car production, jobs and economic value, as local EV demand dampens while foreign car and battery manufacturers grow their technology lead and export into Europe. In this scenario, Europe will see:

-

A further decline in automotive value-added of €90 billion by 2035 and the loss of up to 1 million jobs compared to 2025.

-

A loss of two-thirds of the planned battery investments and jobs, primarily by homegrown European companies, with knockdown effects on adjacent battery component, mineral processing and recycling industries.

-

A loss of €20 million in charging market value in 2035 alone, with a cumulative loss in the charging industry of €125 billion over the 10 years.

Only making Europe’s electric car industrial leadership a priority across climate and industrial policies will help maintain the automotive sector’s overall economic contribution, minimise job losses from the global shift away from the combustion engine and secure new quality jobs in the strategic sectors dependent on Europe’s EV demand. Achieving this requires:

-

1

Maintaining the 2030-2035 car CO2 targets in the upcoming regulatory review, flanked by EU-wide measures to support demand.

-

2

Introducing production aid for EV batteries in both EU and national funding streams, alongside incentives to source EU-made components and materials.

-

3

Implementing the EU Alternative Fuels Infrastructure Regulation and electricity market reforms and grids action plans to speed up charger roll-out and grid connections and permitting.

-

4

Mainstreaming social conditionality for quality jobs, and strengthening technology and skills transfer provisions in foreign direct investment.

Part 1

Introduction

The automotive industry, and particularly car production, has historically been a foundation of the European economy. T&E estimates that the business contributes around €330 billion to the European GDP, and more than 3 million people are employed, directly or indirectly, in the car or components manufacturing sector. Nonetheless, their internal combustion engines continue to be a significant source of pollution, emitting 452 Mt CO₂ in the EU in 2023 alone (approximately 10% of total emissions), underscoring the urgent need to transition to electric vehicles.

As Europe stands at the crossroads of a low-carbon transition, the automotive sector’s contribution to GDP will hinge critically on the industrial policy choices adopted today. While a strong industrial policy will solidify the electric future of road transport and provide regulatory certainty for companies to invest in EVs, batteries, and chargers, inaction or even setbacks will allow foreign competitors to grow larger and erode their market share.

This report provides a comprehensive overview of Europe’s electric vehicle (EV) transition and its associated value chain, drawing together current projects in car manufacturing, battery gigafactories, critical minerals refining and recycling across the continent. We examine how varying rates of production growth and levels of electrification will influence GDP and employment under three distinct scenarios. One chapter is dedicated to the growing charging infrastructure sector, its economic value and employment potential across equipment manufacturing, electricity sales, software and support services. Finally, we propose a suite of targeted industrial policies that would enable Europe to achieve its most ambitious pathway: one in which the region not only restores its pre-pandemic production capacity and reclaims competitiveness against international rivals but also accelerates the shift to zero-emission transport and decarbonises its automotive sector.

This study builds upon and extends T&E’s May 2024 publication, which concentrated primarily on batteries and their upstream supply chain. Throughout the following chapters, we frequently reference this earlier work for foundational data and insights, while broadening the analysis to encompass the full spectrum of EV-related industrial activity. We aim to equip policymakers, industry stakeholders and civil society actors with the evidence and recommendations needed to secure Europe’s leadership in the global EV market.

Part 2

Electric vehicles

In this chapter, we assess the progress of the battery-electric vehicle (BEV) transition from the perspective of industry capacity. T&E examines whether Europe’s manufacturers are prepared to ramp up clean-vehicle output sufficiently to meet the continent’s decarbonisation goals, and what that scale-up will mean for economic value and employment. Our emphasis on production reflects not only the imperative to green the European car fleet with locally made products, but also the ambition to boost exports and support global uptake of zero-emission transport. The key question is: is Europe ready for this challenge?

Readers should note that, throughout this report, we use “BEVs” and “EVs” interchangeably, in contrast to “non-BEVs” or “ICEs” (internal combustion engines). Although the broader EV definition often includes plug-in hybrids (PHEVs), we group PHEVs with ICEs here, since their emissions performance remains significantly worse than that of fully electric vehicles.

Unlocking €16 billion in EV investment

Around 1.8 million BEVs were produced in Europe in 2024 (including the EU, UK, EFTA and Serbia, T&E calculations), very close to those sold in the same year (2 million). Germany leads the way with 1.2 million BEVs produced, followed by France with 330,000. Based on the current EU regulation on car CO2 standards, the compliance is expected to require 9.6 million in 2030 (replacing ICE manufacturing). Hence, although considerable production capacity already exists, significant expansion must occur to avoid losing market share to imports, as companies producing abroad capture the market opportunity.

To gauge the true scale and maturity of the electric-vehicle manufacturing transition, T&E investigated the status of the newest EV production projects announced by domestic and foreign carmakers in Europe (in addition to the existing EV facilities operating today). The new pool looked at here includes all the publicly announced investments for brand new factories or upgrading of existing ones, leaving out those that have already been fully realised, as well as those gradual upgrades that were not officially announced.

Looking at new EV projects expected to come online explains why Germany has zero projects in the map below e.g., as EV production ramp-up in the country has already started and no new plants are expected in the next few years. This allows us to assess the potential new capacity to produce EVs, as well as the associated investment and job creation, under different future outlooks.

Out of the thirteen new projects in scope here, five consist of greenfield plants, while the remaining eight involve the repurposing of existing assembly lines. If all these projects come to life, Europe will increase its existing capacity by at least 2.1 million electric vehicles annually, potentially bringing total production to 5.1 million units already in 2027, enough to keep up with the rising demand. This would come on top of the roughly 1.8 million EVs produced across Europe in 2024. Note that some projects do not distinguish between purely battery-electric and hybrid vehicles, so these figures might still include some plug-in hybrid (PHEV) production.

However, some projects in the list risk being delayed or even cancelled due to the uncertainty around future market perspectives. Whether these will move on or not depends on many factors, including the policy environment (EV market, industrial measures, etc), which currently lacks regulatory certainty and comprehensiveness. This of course does not mean that the existing EV facilities are completely safe, as a lack of an EV market and industrial policy can similarly mean they too will have to ramp down or even close.

T&E evaluated all thirteen new projects against four critical criteria: project status (delayed, started or in testing), construction status (not started, underway or completed), site location definition (yes/no), and public funding commitment (yes/no). Based on these criteria, the projects were classified into three risk categories - low, medium and high risk - reflecting whether the investment is at risk or likely to be completed.

The low-risk cohort comprises five projects that have secured final investment decisions, are either under construction or completed, and are set to start production in 2025, including two brand new plants: BMW in Hungary and Volvo in Slovakia. Stellantis (Serbia), Volkswagen and Chery (Spain) are instead converting existing facilities to expand their BEV production against old polluting vehicles.

Together, they will deliver 550,000 EVs per year and require around €4.8 billion of investment, creating at least 5,550 jobs. These flagship facilities demonstrate that, where regulatory certainty exists, industry is ready to mobilise large-scale production at pace: all these projects were announced in 2022 or earlier, before the current pushback against the EU 2035 car CO2 regulation.

Five projects (one new build and four conversions) fall into the medium-risk bracket. These initiatives have made significant progress on two or three of our criteria, typically with sites secured and financing in place, but are still at risk of stopping everything if the economic or political conditions change abruptly. Collectively, they account for 1.2 million EVs of annual capacity and €9.3 billion in planned investment, and support 11,000 jobs. The new BYD plant in Szeged, Hungary, accounts for almost half of the total investment (€4 billion) and is the largest project in our list, followed by the Seat-Volkswagen plant in Spain that is being reconverted (€3 billion). The JLR group and Nissan are upgrading their facilities in the UK and expect to produce 250,000 EVs combined, the same as Volvo in Gothenburg.

The remaining three projects (two new plants and one conversion) are designated high risk. All are in the early development phase with uncertainties around final investment decisions or the construction start date. The Izera/ElectroMobility project in Poland, for instance, was supposed to give birth to the first BEV production line in the country. However, the project has been paused and ElectroMobility Poland now intends to contribute to the creation of a new European brand, producing cars in Poland. It is unclear what will be the impact of this approach in terms of investments, job creation and technology transfer. The planned investment was nearly €1.4 billion and aimed at producing 200,000 electric cars per year. Similarly, BMW decided to pause the €700 million-worth conversion of its Mini factory in Oxford. We also included the recently announced JMEV plan to build a new factory in Serbia, as the very early stage of the process makes it highly susceptible to disruptive events. JMEV is a joint venture between Renault and the Chinese Jiangling Motors.

By quantifying capacity and investment under each risk tier, our research underscores how regulatory clarity and strong industrial policies translate directly into concrete factory projects. The low-risk cluster exemplifies best practice: projects are already locked in and close to starting production. The medium-risk group, though promising, teeters on swinging market conditions. And the high-risk tranche highlights the opportunities we stand to lose without decisive action, as wars and tariffs can discourage investments in innovative technologies. This is why European policymakers must act now: ensuring consumers' demand, solid incentive schemes, and protection from unfair foreign competition will give carmakers a clear direction for the future even in such a complex and fast-paced geopolitical context.

Production and value

More regulatory certainty has been shown to bring more EV investments, which in turn means higher production. Going beyond individual EV projects, this section estimates the possible overall car production trends in Europe to 2035.

The chart below shows the different trajectories of car production in Europe until 2035 under three possible scenarios. In the industrial policy or best-case scenario, the current CO2 standards are reinforced with measures to prioritise the production of made-in-Europe vehicles and components, facilitate investments in clean tech manufacturing and demand-side policies to support the EV market. The current policies scenario assumes the CO2 standards stay, leading to some market signal to invest in EV production as demand grows, but no further industrial policy is put in place. The low ambition scenario shows the case where the regulation is watered down to a 90% CO2 reduction target in 2035 and no new industrial policy is set. The reader should note that these scenarios represent T&E’s understanding of the current market trend, and are not to be intended as the exact and only consequences of the set policies attached to them.

One reason that Europe is not recovering its pre-COVID production levels as quickly is due to carmakers’ shift to the “value over volume” strategy: they chose to produce more SUVs and premium cars, on which they have higher profit margins, while cutting the production of smaller vehicles which are less profitable.

This choice implied a delay in investing and scaling up battery-electric cars (BEVs) which, as a relatively new technology, is still giving carmakers lower margins compared to petrol and diesel cars, while other countries like China and the US are moving fast in that direction. A failure from EU institutions to marshal coherent industrial policies that spur EV developments does not help solving the issue. With scant incentives for cleantech, be it batteries or charging components, serious state-aid design shortcomings and the absence of safeguards on imports and foreign investment, European manufacturers struggle to compete on scale, investment and technology, leaving factories under-utilised and market leadership slipping abroad.

This creates a competitiveness gap with other countries, mainly China, that could jeopardise the continent’s historical leadership in car manufacturing. This is why, under the current policy environment, production is expected to grow slowly and reach 14.5 million cars in 2035, a slight recovery from the past five years but still 9% lower than the 2010-2019 average. For the same reason, production drops even further in the low ambition scenario. Watering down the CO2 standards will slow down BEV demand and therefore investments even further, setting Europe’s production at the current declining level and condemning it to a residual role in the global car market.

Europe’s only long-term solution to address its drop in car production – while keeping climate ambitions – is to accelerate BEV investment along the entire value chain.

CO2 regulation is an important stimulus for EV demand, but it will not increase production alone. The real difference can be made by a strong, comprehensive industrial policy that secures a large-scale EV value chain in Europe. This must support investment in made-in-Europe cleantech through state aid at the national and EU funds such as the Innovation Fund, incentivise the use of local components and materials, and establish precise conditionalities for foreign investment that add significant value to the European economy. Strengthening the CO2 emission reduction targets with these measures can allow production to rise until the pre-COVID levels, reaching 16.8 million vehicles in 2035. This manufacturing renaissance brought by strong EV and industrial policies would generate high-quality jobs, attract green capital, and reinforce Europe’s strategic autonomy in clean mobility, driving a sustained upward trajectory in GDP contribution throughout the projection period. A mandate for large corporate fleets to purchase electric vehicles by 2030 will secure additional internal demand and act as a further guarantee for carmakers to increase their production of clean vehicles.

To show the impact on the European economy, we then calculated the car industry’s Gross Value Added (GVA) in each scenario. This indicator reflects the sector’s monetary value realised in Europe - i.e. excluding components manufactured elsewhere. GVA is especially important when part of an industry’s value chain occurs abroad, as is currently the case with electric vehicles. If one simply looks at gross turnover (total sales), then the full price of imported components is counted, even though that revenue flows overseas. By contrast, GVA strips out the cost of those imports and focuses on what is produced domestically. This gives policymakers and analysts a clearer picture of how many jobs, how much income and how much tax revenue really accrue at home, helping to target industrial policy, investment incentives and skills-training programs toward strengthening the local economy. Note that we only include passenger car production and its upstream value chain. Other road vehicles such as trucks and vans, as well as the downstream value chain, are not in scope.

Under the industrial policy scenario, where the European Union becomes a premier hub for electric vehicle production, the sector’s value-added could surge by nearly 11% above 2025 levels in the next ten years. New policies will push carmakers to scale up BEV production while investing in a fully European value chain. As around 25% of the electric value chain is currently located outside Europe, compared to only 10% for combustion engines, securing domestic battery gigafactories and advanced component suppliers is key to reducing this foreign dependence and increasing European value and jobs. This will also allow for reducing costs and regaining competitiveness against foreign players.

In the current policies scenario, the automotive sector’s value-added struggles throughout the whole period, and without fully internalising the BEV value chain, it will decrease by 4% in 2030. Without deeper industrial coordination, Europe risks outsourcing critical battery production to third-country suppliers, capping the full industrial and economic benefits of electrification.

Under the low ambition scenario, policy inertia and fragmentation prevail. Weaker regulation and the growing competition lead to a decreasing trend of car production until roughly 11.4 million units per year. Europe thereby misses a generational opportunity: the automotive sector’s value-added decreases significantly by 27%. This stasis undermines decarbonisation goals and sacrifices long-term competitiveness and high-value employment.

Jobs

Jobs represent the most sensitive issue in Europe’s shift to electric mobility. Understandably, many stakeholders worry about employment losses given the fact that EVs require significantly fewer direct labour inputs per vehicle than their ICE counterparts, owing to simpler powertrains with fewer moving parts, and reduced demand for complex engine machining. Job losses have already been recorded in Europe’s automotive supply chain in the last five years. While the transition to electric vehicles comes with challenges in preparing the workforce, a significant threat to jobs lies not in electrification itself but in the hesitation to embrace it fully through a comprehensive policy agenda: as long as Europe questions its current 2030 - 2035 CO2 targets and lacks the accompanying industrial and demand policies - production volumes will stagnate and jobs will vanish. Conversely, a decisive policy pivot toward EVs, backed by targeted production incentives, infrastructure investment and skills training, can help drive higher output and safeguard the jobs we depend on.

Estimating the future of automotive jobs is certainly a difficult task. Several studies tried to investigate it with disparate approaches, yielding disparate results - see McKinsey/AVERE (2024), BCG and T&E (2023), BCG (2021), CLEPA (2021) in the bibliography. While they all highlight the job losses occurring in the combustion engines’ manufacturing, some offer positive outlooks on the potential gains in the battery supply chain and energy production.

Our analysis mostly builds on this literature. It encompasses the full manufacturing value chain (core vehicle components, powertrain modules, battery systems, tyres, and ancillary parts) but excludes sales and aftersales services (such as repair, maintenance, and retail operations). The annex includes more details on the methodology.

Under current labour intensity assumptions, maintaining today’s level of automotive employment - approximately 3.46 million jobs across assembly plants, component suppliers, and battery factories - will require increasing production volumes. In our industrial policy scenario, where coordinated European incentives, targeted investment, and skills‐training programs support EV production, we forecast 3.31 million employees in 2035, 144,000 or 4% fewer workers compared to 2025.

There are two main reasons why this transition can be managed successfully to safeguard the automotive workforce. Firstly, if the number of workers retiring exceeds the number of potential layoffs due to electrification, there is no need for layoffs. Instead, some of the retiring workforce will not be replaced. This was also confirmed to T&E by a few players in the automotive industry. Secondly, the EV transition opens up new businesses and hence job opportunities. As we will show in detail in Chapter 4, charging alone could need up to 130,000 new jobs by 2035 and could fully absorb the lost workforce. Moreover, according to BCG (2021), new jobs in energy production could contribute to an additional 60,000 workers. Although there will be difficulties in managing geographical imbalances and skills mismatch between old and new jobs, the market will stabilise once the transition is complete. Targeted reskilling programs and collective bargaining schemes are crucial to ensure this transition occurs swiftly and smoothly.

Interestingly, more recent studies suggest that labour intensity and demand could even increase in BEV production compared to ICEs. This means that our estimates are to be considered as highly conservative and the number of jobs in each scenario is the minimum achievable for given car production levels.

This outcome underscores the power of proactive policy: as production volumes and value added rise, aggregate labour demand remains almost flat even in case of lower per‐unit staffing requirements. This means that fewer workers produce more cars, i.e. labour productivity increases, and so do the salaries, unless the additional value created is fully channelled into carmakers’ profits. Moreover, the rapid build‐out of domestic battery gigafactories and raw materials networks offers new regional employment hubs, reinforcing Europe’s strategic autonomy.

Different is the situation in the other scenarios, where lingering on mass-scale investments can widen the gap between Europe and other countries as the world’s EV hub. We are witnessing examples of this phenomenon now: some main European carmakers are restructuring their production facilities, having chosen to prioritise the production of high-margin vehicles over high-volume, mass-market ones. Their call to weaken environmental rules seems more like an attempt to keep high margins on ICEs in the short-term without looking at the future.

In the current policies scenario, where existing CO2 standards persist but fail to deepen industrial collaboration or address workforce transitions, labour savings per car translate into a net loss of roughly 530,000 jobs by 2035, or 15% of the current workforce. Plants rationalise headcounts and possibly delocalise production outside Europe to remain competitive.

The stakes rise even higher in a weakened regulatory environment. Should EU negotiators water down the post-2030 CO2 standards - blunting the electrification imperative - production levels will stall. This regulatory backslide path sees a staggering one million job losses by 2035, as both the assembly and upstream sectors contract. The opportunity cost of such inaction would be felt not only in diminished climate ambition but in lost livelihoods for thousands of European families.

Part 3

Investment in the battery value chain

The robustness of Europe’s EV automotive strategy depends on the concrete delivery of hundreds of industrial projects across the EV ecosystem. By far the most valuable EV component - at the heart of the global energy transition race - are lithium-ion batteries, as well as materials that go into them. Battery and related components, raw materials processing, and even end-of-life recycling have become increasingly important for our economy, and a lot of companies have announced investments across Europe.

As done for EV production plants above, T&E comprehensive mapping (explained in the Annex) categorises each initiative by its likelihood of fruition - low, medium or high risk - using four critical milestones: final investment decision (FID) taken, construction underway, site confirmed, and finance from either EU automakers or public bodies. Below, we present the expected production capacities, capital deployment and job creation (when available) at stake in each segment.

When comparing production to future demand, we refer to the T&E forecast for batteries, materials, and components needs in the industrial policy scenario mentioned in the previous chapter. On top of cars, we include light commercial vehicles, trucks and buses, and energy storage systems (ESS).

Battery gigafactories

Batteries are the most valuable component of electric vehicles, representing between one-fifth and one-fourth of the production cost. China was the first country to invest in the sector and is now the market leader with 83% of the global capacity, according to BNEF. Despite the creation of the European Battery Alliance in 2017, the EU was slow to put in place a comprehensive industrial strategy and is now trying to catch up, with both local and foreign companies competing to secure their plants all over the bloc.

Low-risk gigafactories - fully financed and breaking ground, some already operational - will deliver 391 GWh of annual capacity, backed by €39 billion in investment and the potential to create 43,000 skilled posts. ACC plant in Douvrin (France) and Volkswagen PowerCo in Salzgitter (Germany) are among these examples. Medium-risk undertakings, where the construction has not begun mostly due to missing final investment decisions, represent the largest category with 627 GWh in capacity, €48 billion in investment and 47,000 jobs at risk. These include Basquevolt in Spain and Morrow’s expansion of its plant in Arendal, Norway, which is set to more than double its production capacity in 2030. High-risk ventures remain at the concept or permitting phase; they still account for 410 GWh, €21 billion and 37,000 jobs, but hinge on regulatory certainty and robust industrial policy measures to go ahead. ElevenEs’ plan to expand its factory in Subotica (Serbia) to boost its production from the current 0.4 GWh to 22.8 GWh in 2030 belongs to this cluster, as there is no certainty that funding will be provided.

If we look at the net production (i.e. not the theoretical capacity but the actual expected output), we see that Europe could satisfy two-thirds of its domestic battery cell demand in 2030. However, this share drops drastically to 24% if only the low-risk projects succeed (way below the EU’s own target of 40% sufficiency by 2030), and 52% if we add those at medium risk. This value is lower than previous estimates made by T&E, where we showed the best case scenario with the potential to cover all of the battery cell demand from 2027 onwards. While we use a more ambitious EV uptake (including in corporate fleets) in our scenario here compared to the minimum Car CO2 standards, the main reason is that this is a more sober analysis of the actual battery market dynamics at play today with many projects cancelled or delayed due to worse global and EU (e.g. lack of industrial support) dynamics. More details are included in the Annex.

Spain boasts the greatest future gigafactory potential, with planned capacity reaching 244 GWh by 2030. Yet only 13% of that - 32 GWh - is deemed low risk, leaving the vast majority dependent on future political choices. In contrast, Poland and Hungary enjoy far more secure pipelines: their low-risk capacities stand at 115 GWh and 125 GWh, respectively. While Poland does not plan to build more factories soon, Hungary could add another 90 GWh, positioning itself as Europe’s next EV powerhouse.

Major European economies like France and Germany occupy a middle ground, together accounting for over 350 GWh of capacity, of which 130 is classified at low risk. Incumbent countries in the industry could also play a significant role if their medium and high-risk projects come to life. Norway, Serbia and Slovakia currently total only 11 GWh, but could reach a staggering 234 GWh by 2030, contributing to a more autonomous and resilient European EV business.

Europe’s domestic battery projects face a markedly different risk profile compared to their international rivals. While European companies carry a disproportionate share of capacity sitting in medium- and high-risk categories, non-European producers enjoy far greater certainty, with the bulk of their planned output classified as low-risk and already operational or nearing completion. Nearly half of the non-European capacity (279 GWh) lies in the low-risk category, while 28% (191 GWh) is at high risk. On the other hand, European companies face more difficulties, with a worrying 269 GWh (36% of the total planned capacity) facing the severe risk of not being realised, while only 112 GWh (15%) are safe.

This can be explained by a longer track record and expertise in building and operating battery cell factories by South Korean and Chinese companies, as well as more (and lower risk) capital available for investment compared to European start-ups. Having a track record means both investors and automakers trust those non-European players to deliver on their plans, while many nascent European companies are facing more scrutiny in the aftermath of the Northvolt bankruptcy.

Cathode-Active Materials (CAM/pCAM) plants

Cathode Active Materials (CAM) and their precursors (pCAM) are the critical components that make a battery work. They form the positive side of a battery cell and contribute to determining how much energy it holds, how fast it charges, and how long it lasts. They also represent the highest value in a battery cell. CAM/pCAM production is a fundamental step between raw minerals and the finished battery, but Europe currently imports most of these materials (88% CAM and 96% pCAM in 2024, according to our modelling). This creates risks for supply security, price spikes, and carbon-intensive transportation. This also hinders the opportunity to capture a high share of the battery cell value added (they account for around 55% of the battery cell cost). Europe is trying to recover the lost ground and scale up capacity, but are we moving fast enough?

CAM and pCAM facilities are considered at low risk if they are already operational or will start production soon. T&E counts 5 of those plans (located in Germany, Belgium and Denmark) that are expected to handle 66.5 kt of material combined, backed by €850 million and creating 990 jobs. Medium-risk projects are those under construction or with a final investment decision taken. Today, they consist of 14 plants (mostly located in Finland, Poland and Hungary) expected to produce up to 544 kt, requiring €4.5 billion of investment and generating 3,500 jobs. High-risk schemes, representing 161,000 tonnes, €2.2 billion and 1,670 jobs, are less likely to move on and remain contingent on a strong industrial policy framework. These include Umicore and Volkswagen’s joint project in Nysa, Poland.

Despite the number of projects having risen in the last few years, they are by no means sufficient to make Europe a significant player in the industry. Even if all projects go online, only 34% of CAM demand (and 25% for pCAM) will be satisfied in 2030, still below the EU's recently set 40% processing benchmark in the Critical Raw Material Act. In the case where low- and medium-risk projects will be the only successful ones, these shares decrease considerably: 18% for CAM and 9.4% for pCAM.

This delay in scaling up cathode production is worrying. In plain terms, it makes little sense to pour billions into extracting lithium, nickel or manganese - or to build state-of-the-art recycling plants - if we lack the domestic capacity to turn those raw materials into cathode active materials and their precursors. Without a robust network of cathode and precursor facilities, upstream investments will have no local offtake and will be exported to Asia to be turned into CAM and batteries there instead. To unlock the full economic, industrial and environmental benefits of Europe’s mineral investments, we must accelerate and de-risk projects that refine and assemble cathode materials. This will establish a complete supply chain from mine to cell and ensure that every tonne of raw input can flow through to a finished battery.

Recycling facilities

In the medium- to long-term, recycling spent EV batteries will become indispensable for cutting our dependence on newly mined minerals. Unlike the traditional “take-make-dispose” model of combustion-engine vehicles, where fuel is extracted, processed and then permanently lost, lithium-ion batteries can be processed to reclaim critical metals and feed them back into new battery production.

The EU’s Batteries Regulation imposes stringent due diligence and sustainability measures and mandates ambitious recycling quotas and minimum recycled-content thresholds for all EV battery cells on the EU market. Thanks to these rules, Europe’s pool of recyclable battery materials will expand rapidly over the next decade. Early on, most feedstock will stem from manufacturing scrap generated by scaling gigafactories, accounting for roughly 75% of the estimated 100 GWh of available material by 2030 (equivalent to about 10% of that year’s battery demand, see the “Industrial blueprint” report linked above).

According to T&E modelling from the December 2024 report on recycling, Europe can source 11% of its 2030 lithium demand in the current policies scenario from recycling, 12% nickel, 13% manganese and 19% cobalt.

To capture this opportunity, Europe must rapidly build both pre-processing facilities (shredding, sorting and sieving) and, most importantly, downstream recovery plants (hydrometallurgical or pyrometallurgical) to turn this scrap into battery-grade material. A total of 77 projects have been tracked on the continent, of which 37 are already operational. In case all the others get to life, they will be able to process around 500 kt of batteries in the pre-processing stage and over 413 kt of batteries in the material recovery stage in 2030.

In low-risk pipelines, facilities will process 530 kt of end-of-life batteries and manufacturing scrap, ensuring that valuable materials re-enter the supply loop. A medium-risk cohort could expand that figure by 860 kt, deepening Europe’s circular economy and reducing reliance on primary mining. No project was classified as high risk, however, the major horizontal risk faced by all companies is a possible lack of the battery factory scrap pool if gigafactories do not scale as expected.

Although we lack data on specific job or investment figures here, these plants are essential to securing raw-material independence and closing the battery value-chain loop.

Lithium refining

Despite much innovation in EV battery chemistry, most will require lithium in the coming years/decades. The demand for lithium chemicals in Europe is expected to rise from 39 kt lithium carbonate equivalent (LCE) today to 681 kt in 2030.

To date, only 2 lithium refineries are operating: AMG Lithium in Bitterfeld-Wolfen, Germany and LevertonHELM in the UK, aiming to produce 16.6 kt LCE in 2025. The only active extraction site is Guarda, Portugal, where four companies have started operations.

Our research found additional plans for eight refineries, five mines and sixteen integrated plants. However, most of these projects are still in the scoping phase or lack the necessary financial and legal commitment: 96% of the total production capacity is classified as either medium or high risk. Medium-risk expansions - totalling 325 kt, €10.7 billion in investment and 4,000 jobs - could significantly increase Europe’s position in lithium chemicals and cover 48% of the demand in 2030. This category includes two promising projects. The first one is the Sibanye Stillwater & FMG in Finland, whose production can reach 11.2 kt in 2030. The second one is the Vulcan Energy Resources’ “Zero Carbon Lithium” project in Germany, which aims at producing 17.9kt of LCE extracted from geothermal brine with very low land, water and CO2 consumption. It is set to start operations in 2026. Both are integrated projects that will extract and refine lithium at the same time.

High-risk plans, accounting for 213 kt, €3.9 billion and 2,400 jobs, could add another 31% to the 2030 demand coverage, bringing lithium refining to nearly 560 kt, or 82% of the total demand in the industrial policy scenario. These projects face the steepest hurdles in financing, highlighting the urgent need for clear market signals and supportive regulation.

Low-risk operations will yield 20.5 kt of LCE, mobilising €140 million and employing 80 workers. This can account for only 3% of the European needs in 2030, which means that we will still be heavily dependent on imports for such a critical commodity.

Nickel, cobalt, manganese

Nickel, cobalt and manganese form the positive electrode, or cathode, in lithium-ion batteries. Each contributes to battery performance: to simplify, nickel boosts energy density for longer range, cobalt stabilises structure for safety and lifespan, and manganese enhances thermal stability and cost efficiency. These metals combine in cathode materials to store and release power reliably, though the current trend is to increase nickel and manganese at the expense of cobalt. Europe holds only a sliver of the world’s key battery metals compared to major producing nations, which makes it imperative to build a resilient supply chain and boost recycling capabilities.

Three nickel processing plants are active in Finland, and they currently represent the only source of European nickel production. With a combined output of 74 kt of nickel sulphate achievable in 2030, they could cover 18% of the demand in the industrial policy scenario. Among the upcoming projects, the Sakatti mine (Finland) from Anglo American seems to be the most advanced one, although it is still waiting to complete all the necessary steps to start operating. Classified as medium risk in our analysis, it could add 2 kt to our yearly production. High risk projects amounting to 5.6 kt of total production are still in a scoping phase, and it is difficult to tell whether they will be realised without stronger regulatory certainty and industrial policy.

European cobalt production is spread across Finland, Cyprus, France and Norway. However, only the first two countries produce cobalt sulphate, which is what is employed in batteries. They plan to produce 7.4 kt of output in 2030, reaching 16% of the demand. At the moment, there are no plans to increase production or open new plants in the future.

No new manganese projects were announced since T&E’s last year’s “Industrial Blueprint” report. The only active plant is Vibrantz in Belgium, producing around 4.6 kt of manganese sulphate annually. Compared to 2024, no significant updates on the 48 kt/year Euro Manganese project in the Czech Republic are available. Its production is still set to start in 2028, and we classified it as a medium-risk plant. In case it went through, Europe could produce internally around half of its manganese needs in 2030.

Part 4

Charging

Importantly, our modelling also captures the burgeoning charging infrastructure ecosystem. Across all scenarios, the deployment of public and private charging stations, network operation, grid upgrades, and associated services represents a significant business opportunity for the European economy.

Charging points and related value

The number of charging points is calculated from T&E forecast of the electrically chargeable vehicles in the European fleet, including both battery electric (BEV) and plug-in hybrid cars (PHEV), in the same three scenarios we considered for car production. Following the European Commission’s definition, we define a charging point as a structure delivering electric energy to a single vehicle at a time. We distinguish between public and private points, as they play different roles in the charging ecosystem. We then calculate the revenue this business could generate, splitting across the two main segments of the value chain: 1) components manufacturing and installation, and 2) utilisation. Note that this measure is different from the GVA calculations in chapter 2: while before we looked into the amount of money that stays in Europe, here we are considering the total industry’s revenue, without deducting what goes abroad. The annex includes more details on the methodology.

In our industrial policy scenario, where securing the CO2 standards is coupled with strong incentives to support local cleantech production and measures to speed up and simplify the rollout of charging infrastructure across Europe, around 100 million BEVs and 5 million PHEVs will be driving on European roads. As these would account for almost 40% of the total fleet, a deep transformation in the refuelling ecosystem is needed. 53.4 million charging points need to be installed, with an annual growth rate of 17%. The 42.3 million chargers installed in residential buildings constitute the bulk of the new installations, followed by the corporate and destination chargers (located in offices, supermarkets and depots) (9.6 million). Public chargers in urban areas amount to 1.3 million, while points installed in rural areas and on highways are 168,000.

Such a surge in the charging business immediately translates into a significant flow of money into the European economy. By 2035, Europe could increase its current charging value by almost fivefold to €79 billion. While today’s value of €18.4 billion is split roughly equally between production/installation of the equipment and the services related to the utilisation of the charging point (electricity sales, operation and subscription services), the latter ones will lead the value growth in the next 10 years.

The charging network will grow substantially in the other two scenarios, although less than in the industrial policy case. Around 12 million fewer chargers are installed in the current policies scenario over the 10 years analysed, and 15 million fewer in the low ambition one.

Fewer EVs mean fewer chargers, and hence, the business could lose significant value. If no industrial policies are set to support the green transition, the industry’s revenue will reach €62 billion in 2035, or €17 billion less than in the most ambitious scenario. However, this means that a staggering €110 billion potential will be lost over the 10 years across all the charging areas. Numbers get even worse when considering the case where the CO2 standards are revised, as the value in 2035 is €20 billion lower than in the best-case scenario. This translates into €125 billion less revenue over the 10 years.

Jobs

A recent report from P3 and ChargeUp Europe estimates that the EV charging industry has already created over 58,000 charging-related jobs. Based on that, T&E estimates that most of the workforce is employed in the production and setup of the charging equipment, with around 40% employed in the planning and installation phase alone and another 20% in hardware manufacturing. The remaining workers are equally split between electricity sales, operations and related services.

Equipment manufacturing, planning and installation remains the top employer in the Low ambition and current policies scenarios, but its lead narrows in the years as utilisation roles surge, pulled by the electricity sales. In the industrial policy scenario, equipment-related jobs climb from 33,000 today to 88,000 in 2035, while the rise of electricity sales roles increases almost five-fold from 11,000 to 52,000, making utilisation-related posts the top charging employer.

Under current policies, assembly and installation headcount still grows to 73,000, but sales’ ascent slows, reaching 40,000 in 2035. In the low ambition case, a similar number of chargers to the previous scenario means equipment jobs stabilise at 72,000, while the lower utilisation stops electricity sales jobs at 37,000. Across all futures, other services (mostly IT) exhibit the most volatile curve, doubling to 6,000 in the bold Industrial policy world, but remaining at 5,000 or even 4,000 without fresh incentives.

What emerges from this analysis is that, in any case, charging jobs will grow steeply and represent an important opportunity for a wide range of European workers, from installation engineers and electricians to software developers and operators. As most of these jobs (like installation and maintenance services) cannot be outsourced to extra-European countries, they represent a vital growth corridor that policymakers must protect and nurture.

Part 5

Conclusion & policy recommendations

Global geopolitical competition, government efforts to onshore cleantech manufacturing, and trade wars are all impacting Europe’s automotive transformation. The EU and the UK are at a crossroads today, questioning whether they should keep their 2030-2035 zero emission vehicle (ZEV) and car CO2 policies intact amidst strong industry pressure to relax, and hesitating over what industrial policy is necessary to secure local jobs and green business investment.

T&E’s analysis of electric car, battery and charging value chains in terms of capacity, investment, and jobs shows that only a combination of ambitious EV policy and strong industrial and demand measures would allow Europe to reap the geoeconomic benefits of the automotive transformation. While the 2035 regulations create the imperative investment certainty, industrial measures ensure the case for local manufacturing and supply chain.

If the EU rolls back its 2035 Car CO2 standard, while also failing to put in place additional industrial policy measures, it would lose €11 billion investment in EV manufacturing, fail to secure 580 GWh of battery production (equivalent to an investment of €72 billion) and lose an additional €125 billion in GDP contribution from the charging business over the 2025-2035 period. This is the opportunity cost of keeping the current flagship Green Deal policy in place.

On the other hand, complementing the 2035 ZEV decision with targeted industrial measures around European preference, production aid and EV demand will see Europe’s EV production tripling already in 2030, while making the continent procure 67% of its batteries, 46% of the key battery components, cathodes, and 90% of lithium chemicals by the same date. To fully reap the value of new charging business - with many charging jobs local and not at risk of outsourcing abroad - the EU equally needs to ensure all its member states implement the roll-out targets under the Alternative Fuels Infrastructure regulation. The EU must also implement the grid-related plans under its new electricity market reforms and action plans to make sure slow and cumbersome grid processes do not delay chargers from being installed on time.

Crucially, this is not only about jobs per se, as action is also required to make sure these are quality jobs that Europe gains. So measures to strengthen social conditionalities, employment conditions and worker bargaining power also need to be consistently implemented across EU member states.

But these investments and jobs will not materialise on their own and a set of ambitious climate and industrial policies are key. This is what Europe needs to do:

-

1

Keep the 2030-2035 car CO2 targets intact, focusing instead on key industrial and demand policies to make automotive electrification a success

-

2

Reform EU’s funding and state aid rules to allow targeted production aid (subsidy per output of product) for battery manufacturing, with top-ups for using local components & materials

-

3

Introduce a Made in EU requirement into EV incentives and public funding that rewards the use of local components and materials, which is increased gradually as local cleantech capacity grows

-

4

Introduce technology and skills sharing and local supply chain requirements into strengthened EU’s Foreign Direct Investment (FDI) framework, requiring all EU member states to apply those

-

5

Put in place a comprehensive set of demand-side measures to support the EV market, including demanding corporate fleets to purchase higher shares of zero emission vehicles

-

6

Fully implement the Alternative Fuels Infrastructure Regulation, the Electricity Market Design regulation, as well as the measures from the EU Grids Action Plan to speed up charger roll-out and simplify grid connection and permitting requirements.

-

7

Strengthen social safeguards and their national implementation to ensure automotive transformation brings quality jobs, including in mechanisms supporting production across the EV value chain and in EV purchase incentives, avoiding race to the bottom across member states.

Related Articles

View All

News

What the Electrification Action Plan means for transport

T&E's in-depth review of the EU Commission's Electrification Action Plan

Report

Europe’s waste creates value elsewhere

How the Circular Economy Act can provide the tools to help scale Europe’s recycling industry, in order to secure access to critical minerals.

Press Release

Charging infrastructure has far outpaced EV sales in all but one EU country – analysis

Only Malta falls short on the EU’s fleet-based target for public charging.