Impact assessment of the transition to zero-emission trucks in Europe

T&E commissioned Boston Consulting Group to study the impacts of the transition to zero-emission trucks on the European economy and truckmakers’ global competitiveness.

Click to download the study by BCG and the briefing by T&E.

The European Union is currently reviewing its CO2 standards for heavy-duty vehicles (HDVs), the EU’s key policy to decarbonise road freight transport. To assess the industrial policy contribution of the regulation, Transport & Environment commissioned Boston Consulting Group (BCG) to study the impacts of the transition to zero-emission trucks (ZETs) on the European economy and European truckmakers’ global competitiveness.

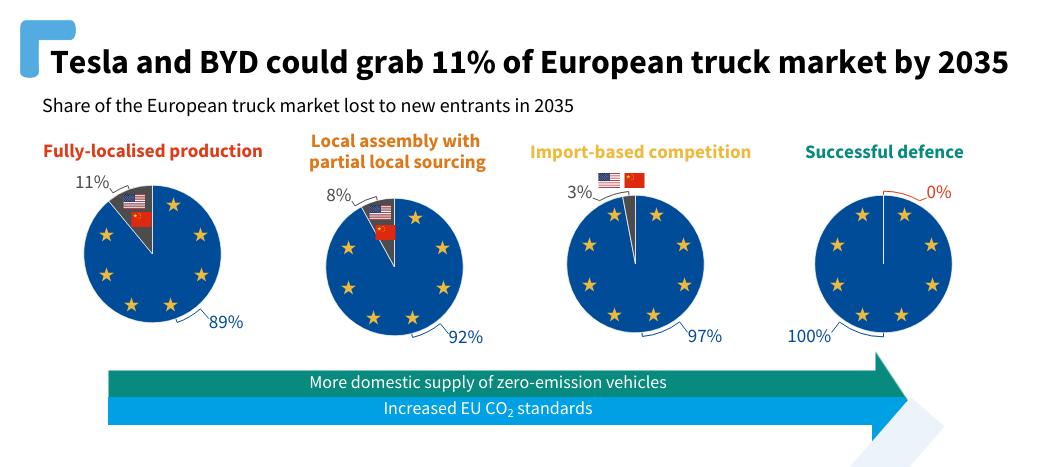

The analysis shows that a slow transition — as would occur under current HDV CO2 standards — puts the European truck industry at risk of losing up to 11% of the EU market to competitors from the United States (US) and China by 2035. For comparison, this corresponds to the EU truck market share of Scania or IVECO today. The exact impact of international competition on the European market depends on the market entry scenario.

As the total cost of ownership (TCO) of battery-electric and fuel cell electric trucks drops below diesel trucks by the late 2020s, European demand for ZETs will surge. But the current HDV CO2 standards would not adequately stimulate supply. Meanwhile, strong policies and subsidies in the US and China would lead them to develop economies of scale faster than Europe. This would open the door to foreign competitors gaining a foothold on the European market through imports, either thanks to lower costs or better technology. Alternatively, strengthening the HDV CO2 targets would help Europe successfully defend its industry by making sure domestic truckmakers keep pace with both international competition and domestic demand and hold on to their market shares.

Stronger HDV CO2 standards are also projected to bring more economic benefits to Europe’s society as a whole, in particular related to employment and gross domestic product (GDP). Compared to current policies, 7,000 net new jobs (+1%) and 10 billion euros in value added (+12%) would be created in the truck manufacturing, infrastructure, and energy sectors under the Commission proposal. Under T&E recommendations, these gains would reach a net increase of 23,000 jobs (+4%) and 27 B€ of value added (+31%).

A strong push for localising battery production in Europe further enhances the benefits of a faster ZET uptake. The number of European jobs per battery-electric truck produced can be increased by ensuring all battery cells are produced in Europe, and onshoring production of cathodes and active materials. With higher battery sovereignty, an additional 9,000 jobs would be gained under the Commission proposal, and 19,000 under T&E recommendations.

Energy sovereignty is the main driver of employment and economic growth. Moving away from diesel trucks will cut our dependence on oil, almost all of which is imported. Truck diesel demand is replaced with domestically-produced electricity — with renewables being the main power source — and hydrogen. The energy transition will greatly benefit the European economy and reduce its vulnerability to volatile global fossil fuel markets.

While the transition will have a net positive impact overall, losses and gains will occur in different sectors. Credible strategies must be in place to ensure workers in internal combustion engine (ICE) manufacturers and suppliers, and diesel refineries are supported with new skills and opportunities. Using the HDV CO2 standards to set the pace of the transition, Europe can predictably determine when efforts to transition ICE employees have to be deployed and ramped up.

However, we shouldn’t be tempted to slow the transition in order to preserve ICE jobs. As discussed above, lagging behind would lead to domestic truckmakers losing market share to foreign competition, resulting in lower truck production volumes overall. The global leadership position in commercial vehicle technology has been traditionally held by Europe. As the world is shifting away from diesel drivetrains, the race to be leaders in ZET technology and produce ZETs cost-competitively is now unfolding.

T&E therefore finds that the HDV CO2 standards are not just crucial for climate. The regulation is also the core industrial policy to defend the competitiveness of the European truck industry. T&E recommends that policymakers raise the ambition of the Commission proposal for the review of the HDV CO2 standards. Namely:

- Strengthen the 2030 CO2 reduction target to -65%, up from -45% in the Commission proposal.

- Set a -100% CO2 reduction target in 2035 for freight trucks, and 2040 for vocational vehicles.

Expand the scope of the regulation to cover all new HDVs, by introducing CO2 reduction targets for vocational trucks and a zero-emission sales target for non-certified vehicles.

Related Articles

View All

Joint letter: EU must reach agreement on zero-emission heavy-duty proposal

Failure to secure an agreement on Weights and Dimensions file would create uncertainty for operators investing in zero-emission heavy-duty vehicles.

Truckmaking giants favour shareholder payouts over investing into the zero-emission transition

In the lead-up to the first-ever EU truck CO2 target in 2025, major truckmakers have come to increasingly prioritise their shareholders over making th...

Joint letter: industry calls for toll exemptions for zero-emission trucks

Leading EU businesses call EU Transport Ministers to implement toll exemptions to accelerate clean freight